For small business owners, especially those looking to expand or update their fleet with heavier vehicles (such as SUVs, pickups, or large vans), there is a strategic advantage in tapping into tax deductions that allow for significant savings. One of the most impactful deductions is the IRS Section 179 provision, which permits qualified businesses to deduct the entire (or a substantial portion of) the purchase price of eligible assets, including heavy vehicles.

Tax deductions reduce your taxable income, effectively lowering your tax liability. Regarding section 179 deduction for vehicles over 6000 lbs, these heavier vehicles often qualify for more favorable depreciation rules than lighter vehicles. Understanding how Section 179 vehicles fit into your tax strategy can help optimize business spending.

This detailed article explores every nuance of the Section 179 deduction for vehicles weighing over 6,000 lbs for the tax year 2025. We will also address the importance of checking an updated section 179 deduction vehicle list 2024 to anticipate changes that may carry into 2025. By doing so, you can stay ahead of the curve, take proactive measures in purchasing and accounting decisions, and comply with IRS section 179 vehicle guidelines.

Below, we break down the full scope of what vehicles qualify for Section 179, how Section 179 works for vehicles, whether Section 179 applies to used vehicles, and the interplay between Section 179 and bonus depreciation. We aim to empower you with a solid foundation of knowledge so you can confidently proceed with your heavy vehicle purchase decisions. Let’s begin.

Updated: May 14, 2025

- Navigating Tax Rules: A Note on Tax Years

- Understanding the Section 179 Deduction

- Understanding Section 179 Deduction for Vehicles

- IRS List of Vehicles Over 6000 Pounds

- Determining if Your Vehicle Qualifies for Section 179 Tax Benefits

- How Section 179 Deduction Applies

- Why Vehicles Over 6,000 Pounds Matter

- Section 179 Vehicle Types – Light vs. Heavy

- Section 179 and Bonus Depreciation: A Powerful Combination for Your Heavy Vehicle Purchase (Tax Year 2025)

- The Linchpin of Vehicle Deductions: Understanding the "More Than 50% Business Use" Rule

- Heavy Vehicle Types: Unlocking Higher Section 179 Deductions Beyond the SUV Limit

- Timing is Everything: What "Placed in Service" Means for Your Vehicle Deduction

- Protecting Your Deductions: Essential Record-Keeping for Business Vehicles

- Keeping Your Deduction: The Rules on Section 179 Recapture

- Section 179 and Your Bottom Line: The Business Taxable Income Limitation

- New or "New-to-You"? Vehicle Eligibility for Section 179 and Bonus Depreciation

- Real-World Scenarios: How Section 179 & Bonus Depreciation Can Work for Your Business (2025 Examples)

- Beyond Federal: A Note on State Tax Rules for Vehicle Deductions

- 2025 Section 179 Deduction Car & Vehicle List for 2025 Purchases

- What Cars & Vehicles Qualify for Section 179

- How Does Section 179 Work for Vehicles?

- Steps to Claim Section 179 for Vehicles Over 6,000 lbs

- How to Claim Your Deduction

- Key Considerations & Potential Limitations

- Section 179 Deduction Vehicle List 2024-2025: Updates and Criteria

- List: Section 179 Deduction Vehicles List for 2025 Cars Over 6,000 lbs

- Frequently Asked Questions

- Key Takeaways

- Conclusion

- Additional Resources

Navigating Tax Rules: A Note on Tax Years

This article primarily focuses on the tax rules applicable to vehicles placed in service in the 2025 tax year. As tax laws evolve, we will also provide context by referencing the rules for the 2024 tax year where helpful for comparison or for those finalizing prior-year tax matters. Always ensure you are applying the rules specific to the year the vehicle was placed in service by your business. The limits and percentages for Section 179 and bonus depreciation can change, so referencing the correct year is essential for accurate tax planning.

Understanding the Section 179 Deduction

1. Definition of Section 179

Section 179 of the Internal Revenue Code allows businesses to deduct the cost of certain assets (most commonly, equipment and software) in the year they are purchased and placed in service. Instead of spreading out depreciation over several years, Section 179 lets you capture substantial deductions upfront. This accelerates your tax savings, significantly benefiting smaller enterprises or those looking to upgrade essential business equipment.

2. Scope and Eligibility

The scope of Section 179 is broad; it covers:

- Tangible personal property used in business (computers, machinery, office equipment).

- Specific improvements to nonresidential real property.

- Vehicles, including passenger automobiles, SUVs, trucks, and vans that meet specific weight and usage requirements.

Heavier vehicles, particularly those with a section 179 weight rating above 6,000 lbs, often enjoy more favorable depreciation limits than lighter passenger vehicles. This is primarily because they are considered essential business equipment.

3. Annual Dollar Limits

The IRS sets an annual maximum deduction limit for Section 179 each tax year. While the threshold can vary based on inflation adjustments and legislative changes, it often hovers in the six figures. For instance, the limit has been over $1 million for all qualified purchases in past years. If you purchase a qualifying vehicle for $60,000, you can often deduct that amount in the year of purchase—provided you meet the relevant criteria.

Note: High-cost vehicle purchases can still be subject to certain “luxury auto limitations,” but heavy vehicles over 6,000 lbs usually face fewer restrictions. Nonetheless, you should always confirm the maximum allowable deduction for any given year by checking the official IRS guidance.

Understanding Section 179 Deduction for Vehicles

If you’re a business owner or self-employed individual looking for cost-saving opportunities, the Section 179 Deduction Vehicle List 2024-2025 is a crucial resource. Under Section 179 of the tax code, eligible businesses can deduct the full purchase price of qualifying equipment and vehicles in the year they are put into service, rather than depreciating them over time. This deduction can provide immediate tax benefits, particularly for large or heavy vehicles.

IRS List of Vehicles Over 6000 Pounds

Before you decide which vehicle to purchase, consult the IRS list of vehicles over 6000 pounds. This list helps you determine if your chosen make and model meets the weight requirement:

- Verify your vehicle’s Gross Vehicle Weight Rating (GVWR) to confirm it meets the 6,000-pound limit.

- Find the IRS list of vehicles over 6000 pounds (PDF) on the official IRS website or consult your tax advisor for guidance.

Determining if Your Vehicle Qualifies for Section 179 Tax Benefits

Many business owners ask if there’s an official IRS list of vehicle models that qualify for the Section 179 deduction. The short answer is no; the IRS does not publish a specific list of makes and models. Instead, qualification hinges on meeting particular criteria, primarily the vehicle’s Gross Vehicle Weight Rating (GVWR) and design characteristics.

What is GVWR and Where Do You Find It?

GVWR stands for Gross Vehicle Weight Rating. It is the maximum allowable total weight of a fully loaded vehicle, including the vehicle itself, passengers, and cargo. The vehicle manufacturer sets this weight.

You can typically find your vehicle’s GVWR:

- On the manufacturer’s label, it is often located on the inside edge of the driver’s side door (door jamb).

- In the vehicle’s owner’s manual.

- On the manufacturer’s official website for the specific model and year.

For Section 179 purposes, we generally look at vehicles with a GVWR of over 6,000 pounds. However, simply meeting this weight threshold is just the first step. The type of vehicle and its features also play a crucial role in determining the extent of the Section 179 deduction available, which we will explore in more detail. Verifying the GVWR for the specific vehicle you purchase is essential, as ratings can vary between different configurations of the same model.

How Section 179 Deduction Applies

Once you’ve determined a vehicle has a Gross Vehicle Weight Rating (GVWR) over 6,000 pounds, the next step is to understand how the Section 179 deduction applies. Not all heavy vehicles are treated the same. The tax rules differentiate primarily between heavy Sport Utility Vehicles (SUVs) and other heavy vehicles like certain trucks and vans.

Key Deduction Limits for Vehicles (Tax Year 2025):

- Heavy SUVs: For new or used sport utility vehicles with a GVWR above 6,000 pounds but not more than 14,000 pounds, and placed in service in 2025, the Section 179 deduction is limited to $31,300. (For comparison, this limit was $30,500 for vehicles placed in service in 2024). This specific limit for SUVs means that even if the vehicle costs more, you cannot deduct more than this amount under Section 179 for that SUV.

- Other Heavy Vehicles: Certain trucks, vans, and other heavy vehicles with a GVWR over 6,000 pounds that are not subject to the SUV limitations (due to their design and how they are used for business) can potentially qualify for a much larger Section 179 deduction – up to the overall Section 179 limit of $1,250,000 for 2025 (provided total qualifying equipment purchases do not exceed the phase-out threshold of $3,130,000). We will detail the characteristics of these vehicles in a later section.

It’s essential to remember the “more than 50% business use” rule, which we’ll cover in depth. If a vehicle isn’t used more than 50% for qualified business purposes, it generally won’t qualify for the Section 179 deduction.

Why Vehicles Over 6,000 Pounds Matter

You might wonder why the 6,000-pound Gross Vehicle Weight Rating (GVWR) is such a key figure in business vehicle tax deductions. The primary reason is that vehicles exceeding this weight threshold can qualify for more favorable depreciation and expensing rules, like Section 179, compared to lighter passenger vehicles.

Bypassing Stricter “Luxury Auto” Limits

Lighter passenger automobiles (those typically under 6,000 lbs GVWR) are often subject to what are known as “luxury automobile depreciation limits.” These rules significantly restrict the amount of depreciation, including Section 179 and bonus depreciation, that can be claimed each year, regardless of the vehicle’s cost or percentage of business use.

By choosing a vehicle with a GVWR over 6,000 pounds that is used primarily for business, your business may be able to:

- Deduct a larger portion of the vehicle’s cost in the first year through Section 179 (up to certain limits, as discussed) and bonus depreciation.

- Accelerate the recovery of the vehicle’s cost over a shorter period than would be allowed under the luxury auto rules.

This distinction allows businesses investing in heavier vehicles—which are often necessary for specific operational needs (like hauling equipment, transporting goods, or carrying a large number of passengers)—to receive a more immediate tax benefit, thereby improving cash flow.

However, it’s crucial to understand that simply being over 6,000 pounds GVWR doesn’t automatically grant an unlimited deduction. As we’ve discussed, different types of heavy vehicles (like SUVs versus certain trucks and vans) have different Section 179 limitations, and all deductions are contingent upon meeting the business use requirements.

1. Weight Criteria and Tax Advantages

Under IRS regulations, there are distinctions between passenger automobiles under 6,000 lbs and heavy vehicles exceeding this threshold. Lighter passenger automobiles are subject to “luxury auto” limits that cap their first-year depreciation deductions to relatively modest amounts. In contrast, if a vehicle’s Gross Vehicle Weight Rating (GVWR) is above 6,000 lbs, businesses can often deduct a higher portion of the vehicle’s purchase cost in the year of acquisition via Section 179.

Essentially, the heavier the vehicle (up to certain limits), the more beneficial it can be from a tax standpoint. This is why savvy small business owners often seek out SUVs, trucks, and vans surpassing 6,000 lbs.

2. Business-Use Requirement

Owning a heavy vehicle does not entitle you to a complete Section 179 deduction. The vehicle must be used more than 50% of the time for business purposes. Accurate, up-to-date mileage logs and records are essential. If, in subsequent years, your vehicle’s business-use percentage falls below 50%, the IRS can enforce “recapture,” meaning you may have to pay back some of the initial tax benefits.

3. Aligning Vehicle Choice with Business Needs

You should only purchase a vehicle over 6,000 lbs if it aligns with your business operations. For instance:

- A construction firm may need a heavy-duty truck for hauling materials.

- A catering company may rely on larger vans or SUVs for transporting supplies.

- A professional services firm may choose an SUV for client transport, especially if the roads or conditions require an off-road-capable vehicle.

Ensuring that your choice suits your operational demands strengthens your compliance posture and helps justify the more favorable deduction.

Section 179 Vehicle Types – Light vs. Heavy

Section 179 of the Internal Revenue Code allows businesses to deduct the full purchase price of qualifying equipment or vehicles in the year they are placed into service rather than depreciating them over time. This provision encourages businesses to invest in equipment and vehicles by providing immediate tax relief.

Light Section 179 Vehicles (GVWR under 6,000 pounds)

- Eligibility: Passenger cars, crossover SUVs, and small utility trucks with a Gross Vehicle Weight Rating (GVWR) under 6,000 pounds.

Deduction Limits for 2024:

- Base Section 179 Deduction: Up to $12,200.

- Additional Bonus Depreciation: An extra $8,000 is available, bringing the total possible deduction to $20,200.

Deduction Limits for 2025:

- Base Section 179 Deduction: Up to $12,200.

- Additional Bonus Depreciation: An extra $8,000 is available, bringing the total possible deduction to $20,200.

Heavy Section 179 Vehicles (GVWR between 6,000 and 14,000 pounds)

- Eligibility: Full-size SUVs, commercial vans, and pickup trucks with a GVWR between 6,000 and 14,000 pounds.

Deduction Limits for 2024:

- Section 179 Deduction: Up to $30,500 for qualifying vehicles.

- Bonus Depreciation: These vehicles qualify for 60% bonus depreciation in 2024.

Deduction Limits for 2025:

- Section 179 Deduction: Up to $31,300 for qualifying vehicles.

- Bonus Depreciation: These vehicles qualify for 40% bonus depreciation in 2025.

Other Section 179 Vehicles (GVWR over 14,000 pounds)

- Eligibility: Vehicles such as large trucks and buses with a GVWR exceeding 14,000 pounds.

Deduction Limits for 2024:

- Section 179 Deduction: These vehicles qualify for the full Section 179 deduction up to the overall limit of $1,160,000.

- Bonus Depreciation: These vehicles qualify for 60% bonus depreciation in 2024.

Deduction Limits for 2025:

- Section 179 Deduction: These vehicles qualify for the entire Section 179 deduction up to the overall limit of $1,250,000.

- Bonus Depreciation: These vehicles qualify for 40% bonus depreciation in 2025.

Key Considerations:

- Business Use Requirement: To qualify for these deductions, the vehicle must be used more than 50% of the time for business purposes.

- Overall Section 179 Limits for 2024 & 2025:

- Maximum Deduction for 2024: $1,160,000.

- Maximum Deduction for 2025: $1,250,000.

- Phase-Out Threshold for 2024: The deduction begins to phase out after $2,890,000 in equipment purchases and completely phases out at $4,050,000.

- Phase-Out Threshold for 2025: The deduction begins to phase out after $3,130,000 in equipment purchases and completely phases out at $4,380,000.

It’s important to note that tax laws can change, and individual circumstances vary. Therefore, it’s advisable to consult with a tax professional or refer to the latest IRS guidelines to understand the specific implications of your situation.

Section 179 and Bonus Depreciation: A Powerful Combination for Your Heavy Vehicle Purchase (Tax Year 2025)

While Section 179 offers a substantial upfront deduction for qualifying heavy vehicles, it’s not the only accelerated depreciation benefit available to businesses. Bonus depreciation is another powerful tool that can be used, often in conjunction with Section 179, to maximize your tax savings in the year you place a vehicle in service.

What is Bonus Depreciation?

Bonus depreciation allows businesses to deduct a percentage of the cost of qualifying new and used assets (including vehicles) in the first year they are placed in service. Unlike Section 179, which has an annual dollar limit and a phase-out threshold, bonus depreciation generally does not have these limitations.

- For qualifying property placed in service in tax year 2025, the bonus depreciation rate is 40%.

- (For comparison, for property placed in service in 2024, the rate was 60%.)

How Section 179 and Bonus Depreciation Work Together:

Businesses often use Section 179 and bonus depreciation in a specific order to maximize their first-year deductions for a qualifying heavy vehicle:

- Apply Section 179 First: You can elect to expense a portion of the vehicle’s cost using the Section 179 deduction, up to the applicable limit (e.g., $31,300 for a heavy SUV in 2025, or up to the full cost for other qualifying heavy vehicles, subject to the overall $1,250,000 Section 179 limit for your business).

- Then, Apply Bonus Depreciation: After applying Section 179, you can then claim bonus depreciation on the remaining adjusted basis of the vehicle. For 2025, this would be 40% of the basis remaining after any Section 179 deduction.

- Finally, Regular MACRS Depreciation: Any basis remaining after Section 179 and bonus depreciation is then depreciated over the vehicle’s regular MACRS (Modified Accelerated Cost Recovery System) recovery period (typically 5 years for cars and trucks).

Key Differences and Considerations:

| Feature | Section 179 | Bonus Depreciation |

|---|---|---|

| Annual Deduction Limit | Yes ($1,250,000 for 2025, vehicle type limits apply) | No general dollar limit |

| Business Income Limit | Yes (deduction cannot exceed net business income) | No (can be claimed even if business has a net loss) |

| Purchase Phase-Out | Yes (starts at $3,130,000 in purchases for 2025) | No |

| Property Eligibility | New and “new-to-you” (used) | New and “new-to-you” (used) |

| Election | Taxpayer elects to take it (or not) | Applies automatically unless taxpayer elects out |

| State Tax Conformity | Varies by state | Varies by state |

The Future of Bonus Depreciation: A Scheduled Phase-Down

It’s important for businesses to be aware that the bonus depreciation percentage is scheduled to decrease in the coming years under current tax law:

- 2025: 40%

- 2026: 20%

- 2027 and beyond: 0%

This phase-down makes strategic planning for significant asset acquisitions, including heavy vehicles, increasingly important if you wish to take full advantage of bonus depreciation before it potentially expires.

Understanding how to best utilize Section 179 and bonus depreciation requires careful consideration of your business’s overall financial picture, taxable income, and planned equipment purchases. Consulting with a tax professional can help you optimize these valuable deductions.

The Linchpin of Vehicle Deductions: Understanding the “More Than 50% Business Use” Rule

Claiming significant tax deductions like Section 179 or bonus depreciation for a vehicle hinges on one absolutely critical factor: the vehicle must be used more than 50% for qualified business purposes. This is not just a guideline; it’s a strict Internal Revenue Service (IRS) requirement. If your business use of a vehicle does not meet this threshold in the year you place it in service, you generally cannot claim Section 179 or bonus depreciation for that vehicle.

What Qualifies as “Business Use”?

Business use generally involves driving the vehicle for activities directly related to your trade or business. Examples include:

- Driving to meet with clients or customers.

- Traveling between different business locations.

- Transporting goods, materials, or equipment for your business.

- Running business-related errands, such as trips to the bank or office supply store.

Commuting miles—driving from your home to your primary place of business and back—are generally considered personal use, not business use, and do not count towards the more than 50% requirement. There are some exceptions to the commuting rule, for instance, if your home is your principal place of business and you are traveling from there to another work location.

Calculating Your Business Use Percentage:

To determine your business use percentage, you need to track the total miles the vehicle was driven during the tax year (or the portion of the year it was in service) and the total miles driven for business purposes.

The formula is:

Business Use Percentage = Total Business Miles Driven / Total Miles Driven (Business + Personal) × 100%

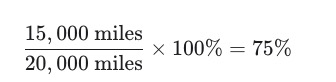

For example, if you drove a vehicle 20,000 total miles in a year, and 15,000 of those miles were for qualified business purposes, your business use percentage would be: 15,000 miles / 20,000 miles × 100% = 75%

In this scenario, since 75% is more than 50%, the vehicle would meet the business use test for Section 179 and bonus depreciation eligibility for that year. The actual deductible amount would then be based on this 75% business use. For instance, if you were eligible to deduct $10,000 under Section 179 based on the vehicle’s cost, you would actually deduct $7,500 ($10,000 * 75%).

Why Meticulous Record-Keeping is Essential:

The IRS requires taxpayers to substantiate their business use claims with adequate records. The best way to do this is by keeping a contemporaneous (meaning recorded at or near the time of travel) mileage log. This log should detail:

- The date of each trip.

- The starting and ending odometer readings or total miles for the trip.

- The destination or purpose of the trip (clearly indicating its business nature).

- The total miles driven for the year (business and personal).

Without proper records, your deductions could be disallowed if your tax return is examined.

Consequences of Business Use Dropping Below 50% (Recapture):

Even if you meet the “more than 50% business use” test in the year you place the vehicle in service, you must continue to monitor its business use percentage throughout its recovery period (typically five years for cars and trucks). If business use drops to 50% or less in any of those subsequent years, you may have to “recapture” (give back) a portion of the Section 179 deduction and any excess depreciation you previously claimed. This means adding the recaptured amount back into your taxable income for that year. We will discuss recapture in more detail in a dedicated section.

Meeting the ‘more than 50% business use’ rule is fundamental. If you are unsure whether your vehicle use will meet this threshold, or how to properly document it, it is wise to consult with a tax professional.

Heavy Vehicle Types: Unlocking Higher Section 179 Deductions Beyond the SUV Limit

We’ve established that vehicles with a Gross Vehicle Weight Rating (GVWR) over 6,000 pounds can offer significant tax advantages. We also noted that heavy Sport Utility Vehicles (SUVs) have a specific, lower Section 179 deduction limit ($31,300 for vehicles placed in service in 2025).

However, certain other heavy vehicles, also with a GVWR over 6,000 pounds, are not subject to this SUV limit and can qualify for a much larger Section 179 deduction—potentially up to the full overall limit of $1,250,000 for 2025 (assuming all other business and equipment purchase limits are met). These vehicles generally have characteristics that distinguish them from typical passenger SUVs.

Here are common examples of vehicles that, if their GVWR is over 6,000 pounds, may qualify for the higher Section 179 deduction:

- Certain Vans and Trucks Designed for Cargo, Not Passengers:

- Classic Cargo Vans: These are typically vans that do not have rear passenger seating. Key features often include:

- A fully enclosed driver’s compartment and an open cargo area (or a cargo area that is separate from the driver).

- No seating behind the driver’s seat, or if there is, it’s minimal and not designed for regular passenger transport.

- Often, these vehicles do not have windows along the sides of the cargo area, or they are designed primarily for loading and unloading goods.

- Heavy-Duty Pickup Trucks with Specific Bed Characteristics:

- Pickup trucks with an interior cargo bed length of at least six feet (72 inches) that is not easily accessible from the passenger compartment may qualify. The key is that the truck is built more for hauling than for passenger comfort.

- Some pickup trucks with beds shorter than six feet might still qualify if they have other features that clearly make them work vehicles (e.g., a chassis-cab design).

- Classic Cargo Vans: These are typically vans that do not have rear passenger seating. Key features often include:

- Vehicles Designed to Seat More Than Nine Passengers:

- Shuttle vans or buses that are designed to seat more than nine passengers behind the driver’s seat can qualify. This is based on the manufacturer’s original design, not aftermarket modifications for passenger capacity.

- Other Specialized Vehicles:

- Vehicles with a specific design for a particular business use, such as an ambulance, hearse, or a heavy-duty vehicle clearly modified for a specific trade (like a dump truck or a tow truck), often qualify for the higher deduction if their GVWR is over 6,000 pounds.

Important Considerations:

- Manufacturer’s Intent and Vehicle Design: The IRS looks at the primary design and use of the vehicle. A vehicle that is clearly designed and marketed as a passenger SUV, even if it’s heavy, will likely fall under the SUV limitations.

- “New to You”: Both new and used vehicles (as long as they are “new to your business”) can qualify.

- State Rules May Differ: Remember that your state may have different rules for vehicle depreciation and Section 179. This article focuses on federal tax law.

Determining whether a specific heavy vehicle qualifies for the higher Section 179 deduction beyond the SUV limit can sometimes be complex. It involves examining the vehicle’s Gross Vehicle Weight Rating (GVWR), its physical characteristics, and its intended use in your business. Suppose you are considering a vehicle purchase and want to maximize your tax benefits. In that case, reviewing the specific vehicle’s attributes with your tax advisor before purchasing is always a good idea.

Timing is Everything: What “Placed in Service” Means for Your Vehicle Deduction

You’ve identified a qualifying heavy vehicle, understand the potential Section 179 and bonus depreciation benefits, and are diligent about meeting the ‘more than 50% business use’ rule. But when can you actually claim these valuable deductions? The answer lies in a key tax term: ‘placed in service.’

Simply purchasing a vehicle is not enough to claim a deduction in a given tax year. The vehicle must be placed in service in your trade or business during that year.

What Does “Placed in Service” Mean?

According to the IRS, property is considered ‘placed in service’ when it is ready and available for its specific assigned function in your trade or business. This means it’s not just sitting on a lot or in storage; it’s prepared and available for active use in your business operations.

Let’s break this down:

- Ready: The vehicle must be in a condition to be used. For example, if it requires significant modifications or installations before it can perform its intended business function, it might not be considered ‘ready’ until those are complete.

- Available: The vehicle must be accessible for use in your business. If you purchase a vehicle late in December but it’s not delivered or prepared for use until January of the next year, it would typically be considered placed in service in that next year.

Examples:

- If you purchase a delivery van on December 20th, have it insured and registered, and make its first business delivery on December 28th, it is clearly placed in service in that tax year.

- If you purchase a truck on December 29th, but it needs special equipment installed that isn’t completed until January 10th of the following year, the truck would likely be considered placed in service in the year the installation is complete and ready for its business function.

Why the “Placed in Service” Date Matters:

The ‘placed in service’ date determines the tax year for which you can claim Section 179, bonus depreciation, and begin regular MACRS depreciation. Even if you pay for a vehicle in one year, if it’s not placed in service until the next, the deduction generally belongs to that next year.

For year-end tax planning, businesses often consider vehicle purchases. It’s crucial to ensure that any vehicle acquired with the intent of claiming a current-year deduction is actually placed in service (ready and available for its business use) by December 31st of that year. Keep records, such as delivery receipts, insurance effective dates, and logs of its first business use, to support your ‘placed in service’ date.

Protecting Your Deductions: Essential Record-Keeping for Business Vehicles

Claiming substantial tax deductions for your business vehicles, such as those under Section 179 or through bonus depreciation, comes with an important responsibility: maintaining thorough and accurate records. The Internal Revenue Service (IRS) requires taxpayers to substantiate their claims for vehicle expenses and depreciation. Without proper documentation, your hard-earned deductions could be at risk if your tax return is ever selected for examination.

Think of good record-keeping as the foundation that supports your tax position. It’s not just about having receipts; it’s about being able to demonstrate the business use and cost basis of your vehicle.

Key Records Your Business Must Maintain:

- Proof of Purchase and Cost Basis:

- Purchase Invoice/Bill of Sale: This document should clearly show the seller, buyer (your business), date of purchase, vehicle identification number (VIN), make, model, year, and the total purchase price. Itemize any additional costs included, such as sales tax, title fees, and delivery charges, as these are generally part of the vehicle’s basis.

- Financing Documents (if applicable): If you financed the vehicle, keep copies of the loan agreement.

- GVWR Documentation: Ensure you have documentation (like a notation on the bill of sale confirmed by the dealer, a copy of the relevant page from the owner’s manual, or a printout from the manufacturer’s website for that specific VIN) showing the vehicle’s Gross Vehicle Weight Rating.

- Evidence of “Placed in Service” Date:

- Keep records showing when the vehicle was ready and available for its intended business use (e.g., delivery receipts, insurance policy effective dates, records of first business use).

- Detailed Mileage Logs (Critically Important for Business Use Substantiation):

- To prove the ‘more than 50% business use’ requirement and to accurately calculate the deductible portion of your vehicle expenses, a contemporaneous mileage log is essential. ‘Contemporaneous’ means the record is made at or near the time the mileage was incurred. Waiting until year-end to recreate a log is not ideal and may not meet IRS standards.

- Your mileage log should include:

- Date of each business trip.

- Starting Point and Destination for each trip.

- Business Purpose of the trip (e.g., “Client meeting with John Doe,” “Supplies pickup from ABC Vendor,” “Site visit to Elm Street project”). Be specific.

- Odometer Readings: Starting and ending odometer readings for each business trip. Alternatively, you can record the total business miles for that trip.

- Total Miles Driven During the Year: Keep a record of the vehicle’s total mileage for the year (e.g., starting and ending odometer readings for the tax year). This helps establish the overall context for your business use percentage.

- Various methods can be used for mileage logging, including manual logbooks, spreadsheets, or GPS-based mileage tracking apps. Choose a method you will use consistently.

- Records of Actual Vehicle Expenses (if using the actual expense method):

- While Section 179 and bonus depreciation relate to the vehicle’s cost, if you are also deducting actual operating expenses (instead of using the standard mileage rate for ongoing expenses after the first year), you’ll need receipts and records for:

- Gas and oil

- Maintenance and repairs

- Tires

- Insurance

- Registration fees and licenses

- Garage rent (if applicable)

- Lease payments (if leasing – though Section 179 generally doesn’t apply to leased vehicles for the lessee)

- While Section 179 and bonus depreciation relate to the vehicle’s cost, if you are also deducting actual operating expenses (instead of using the standard mileage rate for ongoing expenses after the first year), you’ll need receipts and records for:

Why Diligence Matters:

The IRS often scrutinizes vehicle deductions due to the potential for personal use. Complete and accurate records are your best defense. They not only support the deductions taken but also demonstrate your diligence in complying with tax laws.

Store these records securely with your tax documents for at least three to seven years after filing your tax return, as per general IRS record retention guidelines, or longer if specific circumstances apply. Consulting with your CPA can help you establish a record-keeping system that meets IRS requirements and suits your business operations.

Keeping Your Deduction: The Rules on Section 179 Recapture

Claiming a Section 179 deduction provides a significant upfront tax benefit by allowing your business to expense the cost of qualifying property, like a heavy vehicle, in the year it’s placed in service. However, this benefit comes with specific ongoing responsibilities. Suppose you fail to meet these responsibilities during the vehicle’s recovery period, typically the number of years over which it would generally be depreciated, usually five years for cars and trucks. In that case, the IRS may require you to ‘recapture’ or give back a portion of the deduction you claimed.

What is Section 179 Recapture?

Section 179 recapture means that a part of the Section 179 deduction you previously took is added back to your business’s taxable income. Essentially, it reverses some of the tax benefit you received because the property no longer qualifies for the full extent of the initial deduction.

When Does Recapture Typically Occur for Vehicles?

The two most common triggers for Section 179 recapture related to business vehicles are:

- Business Use Drops to 50% or Less:

- As we’ve emphasized, to claim Section 179, the vehicle must be used more than 50% for qualified business purposes in the year it’s placed in service.

- This ‘more than 50% business use’ test must also be met throughout the vehicle’s entire IRS-defined recovery period (usually five years for vehicles).

- If, in any year during that recovery period after the year you claimed the Section 179 deduction, your business use of the vehicle drops to 50% or less, recapture is triggered.

- Early Disposition (Sale, Trade-in, or Conversion to Personal Use):

- If you sell, trade-in, or otherwise dispose of the vehicle before the end of its full recovery period, recapture may occur.

- Similarly, if you convert the vehicle from business use to primarily personal use before the end of its recovery period, this is treated as a disposition for recapture purposes.

How is Recapture Calculated (Simplified)?

The amount of Section 179 deduction that needs to be recaptured is generally the difference between the Section 179 deduction you claimed and the amount of depreciation you would have been allowed to claim under regular MACRS depreciation rules up to the point of recapture.

For example, imagine you claimed a $20,000 Section 179 deduction on a vehicle in Year 1. If, in Year 3, your business use drops to 40%, you would need to calculate how much regular depreciation you would have taken by Year 3. The excess of your $20,000 Section 179 deduction over that calculated regular depreciation amount would be the recaptured amount, which gets added back to your income in Year 3.

The specific calculation can be complex and is reported on IRS Form 4797, Sales of Business Property.

Avoiding Recapture:

- Maintain Business Use: The most straightforward way to avoid recapture is to ensure that the vehicle continues to be used more than 50% for qualified business purposes throughout its recovery period. Diligent mileage logging is key here.

- Understand the Implications of Early Disposal: Before selling or trading in a vehicle for which you claimed Section 179, understand the potential recapture implications.

Recapture rules are in place to ensure that the significant tax benefits of Section 179 are aligned with the property’s sustained use in a trade or business. If your business circumstances change, or if you plan to change how a vehicle is used, it’s wise to consult with your tax advisor to understand any potential recapture consequences.

Section 179 and Your Bottom Line: The Business Taxable Income Limitation

The Section 179 deduction is a powerful tool for reducing your business’s current tax bill by allowing you to expense the full cost of qualifying equipment, including heavy vehicles, in the year of purchase. However, there’s an important cap on the total Section 179 deduction you can claim in any given year: it cannot exceed your business’s net taxable income for that year.

What is the Business Taxable Income Limitation?

Simply put, your Section 179 deduction cannot create or increase a net operating loss for your business. The total amount you elect to expense under Section 179 (for all qualifying property, not just vehicles) is limited to the aggregate net taxable income from all trades or businesses you actively conduct during the tax year.

- Calculating Taxable Income: For this purpose, taxable income is figured before deducting the Section 179 expense itself, any net operating loss carryback or carryforward, and certain other deductions.

- Applies to All Active Businesses: If you own multiple businesses (e.g., a sole proprietorship and an S-corporation you actively participate in), the income (or loss) from all these active ventures is typically combined to determine your overall taxable income limit for Section 179.

Example:

Let’s say your business purchases a qualifying heavy truck for $50,000 and wishes to expense the full amount under Section 179.

- If your business’s net taxable income for the year (before the Section 179 deduction) is $70,000, you can deduct the full $50,000 under Section 179, as it’s less than your taxable income.

- However, if your business’s net taxable income is only $30,000, your Section 179 deduction for that year would be limited to $30,000. You cannot use Section 179 to take a $50,000 deduction and create a $20,000 business loss.

What Happens if Your Deduction is Limited by Taxable Income? The Carryover Provision.

If your Section 179 deduction is limited because it exceeds your business taxable income, the good news is that the disallowed amount is not necessarily lost. Generally, you can carry forward the unused portion of the Section 179 deduction to the next tax year.

In the example above, where the business income was $30,000 and the desired Section 179 deduction was $50,000:

- You would deduct $30,000 under Section 179 in the current year.

- The remaining $20,000 ($50,000 – $30,000) would be carried forward to the following tax year. This carryforward amount can then be deducted in that future year, again subject to the taxable income limitation for that year.

How This Differs from Bonus Depreciation:

This taxable income limitation is a key difference between Section 179 and bonus depreciation. As discussed earlier, bonus depreciation is not limited by your business’s taxable income. You can claim bonus depreciation even if your company has a net operating loss for the year.

Understanding the business taxable income limitation is crucial for effective tax planning. Suppose you anticipate your business income might be lower in a year you plan to make significant equipment purchases. In that case, you’ll want to consider how this limit might affect your Section 179 strategy and whether relying more on bonus depreciation (if available) might be beneficial. It’s always best to discuss these scenarios with your tax advisor.

New or “New-to-You”? Vehicle Eligibility for Section 179 and Bonus Depreciation

When considering the Section 179 deduction and bonus depreciation, business owners have a common question: whether these tax benefits apply only to brand-new vehicles or if used (sometimes called ‘pre-owned’) vehicles can also qualify.

Good News: Both New and Used Vehicles Can Qualify!

For both the Section 179 deduction and bonus depreciation, your business can generally claim these benefits for both:

- New Vehicles: Vehicles that have not been previously owned or used.

- Used Vehicles (or “New-to-You” Vehicles): Vehicles that have been previously owned, as long as the vehicle is new to you and your business.

The “New-to-You” Rule:

The key requirement for a used vehicle to qualify is that your acquisition of it must be its first use by you or your business. This means you cannot claim Section 179 or bonus depreciation on a vehicle that:

- You previously owned personally and are now converting to business use (though regular depreciation rules might apply).

- Your business previously owned, disposed of, and then reacquired.

- Was acquired from a related party (e.g., buying a vehicle from a family member or another business you control, under certain IRS definitions of ‘related party’).

Essentially, the vehicle must be acquired in an arm’s-length transaction, and its use by your business must begin with your acquisition.

Why This Matters for Your Business:

The ability to claim Section 179 and bonus depreciation on qualifying used heavy vehicles provides businesses with greater flexibility. It means you can potentially achieve significant tax savings even when purchasing a more budget-friendly pre-owned vehicle, as long as it meets all other requirements (GVWR, business use, placed in service, etc.). This can be particularly advantageous for small and medium-sized businesses looking to manage cash flow while still investing in necessary equipment.

So, whether you’re eyeing a brand-new truck fresh off the lot or a well-maintained used cargo van, both can be eligible for these valuable first-year expensing and depreciation benefits, provided all IRS conditions are met. Always ensure you have clear documentation of the purchase and that the vehicle meets the definition of ‘new-to-you’ if it’s a used asset.

Real-World Scenarios: How Section 179 & Bonus Depreciation Can Work for Your Business (2025 Examples)

Understanding the rules for Section 179 and bonus depreciation is one thing; seeing how they can impact your business’s bottom line is another. Let’s walk through a few common scenarios to illustrate how these powerful deductions can apply to heavy vehicle purchases made and placed in service in tax year 2025.

For these examples, we’ll assume the business meets the ‘more than 50% business use’ rule, has sufficient business taxable income for any Section 179 claimed (unless otherwise noted), and its total qualifying asset purchases for the year are below the $3,130,000 Section 179 phase-out threshold.

Scenario 1: Purchase of a Heavy SUV

- Vehicle: New heavy SUV

- Cost: $75,000

- Gross Vehicle Weight Rating (GVWR): 6,800 lbs

- Business Use: 100%

Calculation:

- Section 179 Deduction:

- Heavy SUVs (GVWR > 6,000 lbs but not > 14,000 lbs) are limited to a Section 179 deduction of $31,300 for 2025.

- Section 179 Deduction: $31,300

- Remaining Basis for Further Depreciation:

- Original Cost: $75,000

- Less Section 179 Deduction: -$31,300

- Adjusted Basis: $43,700

- Bonus Depreciation (40% for 2025):

- Bonus depreciation is calculated on the adjusted basis after Section 179.

- 40% of $43,700 = $17,480

- Bonus Depreciation: $17,480

- Remaining Basis for Regular MACRS Depreciation:

- Adjusted Basis (after Sec 179): $43,700

- Less Bonus Depreciation: -$17,480

- Basis for MACRS: $26,220

- This $26,220 will be depreciated over the vehicle’s 5-year MACRS recovery period, starting in Year 1. (The first-year MACRS percentage is typically 20% of this amount, so $26,220 * 20% = $5,244 in Year 1 under MACRS).

Total First-Year Deductions for Scenario 1:

- Section 179: $31,300

- Bonus Depreciation: $17,480

- First-Year MACRS Depreciation: $5,244 (20% of $26,220)

- Total Year 1 Deduction: $31,300 + $17,480 + $5,244 = $54,024

This example shows how, even with the SUV limit on Section 179, combining it with bonus depreciation and regular MACRS depreciation can lead to a substantial first-year write-off.

Scenario 2: Purchase of a Qualifying Heavy Pickup Truck (Not Subject to SUV Limits)

- Vehicle: New heavy pickup truck (e.g., with a cargo bed over 6 feet long)

- Cost: $80,000

- Gross Vehicle Weight Rating (GVWR): 7,500 lbs

- Business Use: 100%

- Business Taxable Income: Sufficient to cover the deduction.

- Total Section 179 Property Purchases for the Year: Below the $1,250,000 overall limit and $3,130,000 phase-out.

Calculation:

- Section 179 Deduction:

- Since this truck is not classified as an SUV for Section 179 limitation purposes (due to its design, e.g., long bed), it can qualify for the full Section 179 deduction up to its cost, provided the business’s overall Section 179 limit ($1,250,000 for 2025) is not exceeded by other qualifying purchases.

- The business elects to expense the full cost.

- Section 179 Deduction: $80,000

- Remaining Basis for Further Depreciation:

- Original Cost: $80,000

- Less Section 179 Deduction: -$80,000

- Adjusted Basis: $0

Total First-Year Deductions for Scenario 2:

- Section 179: $80,000

- Bonus Depreciation: $0 (since the basis is $0 after Section 179)

- MACRS Depreciation: $0 (since the basis is $0)

- Total Year 1 Deduction: $80,000

In this case, the business can write off the entire cost of the truck in the first year using Section 179 alone, providing a significant immediate tax benefit.

Scenario 3: Vehicle Purchase with Partial Business Use

- Vehicle: New heavy cargo van (qualifies for full Section 179, not an SUV)

- Cost: $60,000

- Gross Vehicle Weight Rating (GVWR): 8,200 lbs

- Business Use: 70% (This means personal use is 30%. Since business use is over 50%, it qualifies.)

- Business Taxable Income: Sufficient.

- Total Section 179 Property Purchases: Below limits.

Calculation:

- Determine Business Portion of Cost:

- Vehicle Cost: $60,000

- Business Use Percentage: 70%

- Business Portion of Cost: $60,000 * 70% = $42,000

- This $42,000 is the maximum amount eligible for Section 179 and is the basis for calculating bonus depreciation related to business use.

- Section 179 Deduction:

- The business can elect to expense up to the business portion of the cost under Section 179, assuming it doesn’t exceed overall limits. Let’s assume the business elects to take the maximum Section 179 on this vehicle’s business use portion.

- Section 179 Deduction: $42,000

- Remaining Business Basis for Further Depreciation:

- Business Portion of Cost: $42,000

- Less Section 179 Deduction: -$42,000

- Adjusted Business Basis: $0

Total First-Year Deductions for Scenario 3 (Business Portion):

- Section 179: $42,000

- Bonus Depreciation: $0 (since the business basis is $0 after Section 179)

- MACRS Depreciation: $0 (since the business basis is $0)

- Total Year 1 Deduction (for business use): $42,000

Important Note on Partial Business Use:

- Only the business use portion of the vehicle’s cost is eligible for these deductions.

- If, in this scenario, the business had elected to take less than $42,000 as a Section 179 deduction (for example, $20,000), then bonus depreciation and MACRS would apply to the remaining business basis.

- Example if only $20,000 Section 179 was taken on the $42,000 business basis:

- Section 179: $20,000

- Remaining Business Basis for Bonus: $42,000 – $20,000 = $22,000

- Bonus Depreciation (40% of $22,000): $8,800

- Remaining Business Basis for MACRS: $22,000 – $8,800 = $13,200

- First-Year MACRS (20% of $13,200): $2,640

- Total 1st Year Deduction in this alternative: $20,000 + $8,800 + $2,640 = $31,440

- Example if only $20,000 Section 179 was taken on the $42,000 business basis:

These examples illustrate the significant impact these deductions can have. However, the optimal strategy depends on each business’s specific financial situation, overall asset purchases, and taxable income. Professional tax advice is crucial to navigate these rules effectively.

Beyond Federal: A Note on State Tax Rules for Vehicle Deductions

While this article has focused on the federal tax rules for Section 179 and bonus depreciation for heavy vehicles, businesses should remember that state tax laws may not always align with these federal provisions. This is known as ‘state tax conformity.’

Many states conform to the Internal Revenue Code (IRC) to some extent, but they often ‘decouple’ or have different rules for specific deductions, including Section 179 expensing and bonus depreciation. This means that while you might be able to claim a specific deduction on your federal tax return, your state may:

- Not allow the deduction at all.

- Allow a different amount for the deduction.

- Have different income limitations or phase-out thresholds.

For Businesses in Texas: Texas does not have a state corporate income tax or individual income tax. However, Texas does impose a Margin Tax on most taxable entities. The calculation of the Texas Margin Tax has its own specific rules for cost of goods sold and compensation, and federal depreciation deductions like Section 179 or bonus depreciation may not directly reduce your Texas Margin Tax liability in the same way they reduce federal taxable income.

For Businesses Operating in Multiple States: If your business operates in multiple states, the complexity increases, as you’ll need to consider the conformity rules for each state in which you have a tax filing obligation.

Always Consult on State Tax Implications: Due to the variability in state tax laws, it is crucial to consult with a qualified tax professional who understands both federal and your specific state(s’) tax regulations. This will ensure you accurately report and maximize your tax benefits at both the federal and state levels. Do not assume a federal deduction automatically applies to your state tax return.

2025 Section 179 Deduction Car & Vehicle List for 2025 Purchases

Many businesses plan vehicle purchases before the new tax year. If you’re looking at a Section 179 deduction vehicle list 2025 to guide your 2025 acquisitions, you’re anticipating which makes and models will likely remain above 6,000 lbs GVWR. The eligibility often depends on:

- Manufacturer Specifications: They provide a Gross Vehicle Weight Rating (GVWR), which is the maximum loaded weight of the vehicle.

- IRS Updates: The IRS may release annual or periodic updates clarifying specific rules or dollar limitations.

Because automakers frequently adjust their lineups or vehicle specs, it’s vital to verify details with an updated manufacturer’s guide or consult official sources. If, for example, a 2024 model meets the 6,000-lb threshold, the 2025 edition might also do so if the body style or mechanicals haven’t changed significantly. Staying informed ensures you select a vehicle that retains its eligibility under Section 179 vehicle guidelines.

What Cars & Vehicles Qualify for Section 179

1. IRS Criteria

To fall under the beneficial depreciation rules of Section 179, a vehicle must:

- Be used primarily (over 50%) for business.

- Be purchased (not leased) by the business or business owner and placed in service during the relevant tax year.

- If you aim for the more favorable caps, have an appropriate GVWR for heavier vehicles, generally above 6,000 lbs.

Additionally, some vehicles, such as ambulances, hearses, or transport vans, are treated differently due to their specialized nature. However, they still often qualify if used directly in the normal course of business.

2. “New to You” Requirement

Many business owners wonder: Does section 179 apply to used vehicles? The IRS generally permits used vehicles to qualify for Section 179 deductions, provided the asset is “new to you” and meets the other usage and weight requirements. For instance, if you buy a pre-owned pickup truck with a GVWR over 6,000 lbs for your landscaping company and use it for business 70% of the time, you can typically claim Section 179 if all other conditions are met.

3. Special Exceptions

Some heavier passenger automobiles—like SUVs—may still have a maximum allowable deduction slightly lower than full-size cargo vans or massive trucks. Staying updated on exact amounts can help you decide which type of vehicle best aligns with business functionality and potential tax benefits.

How Does Section 179 Work for Vehicles?

1. Immediate Expense Deduction

Under customary tax laws, vehicles must be depreciated (deducted) over multiple years. Section 179 accelerates this process. For heavier vehicles (usually over 6,000 lbs but under 14,000 lbs), Section 179 often allows you to deduct a significant portion (sometimes 100% of the purchase price, up to the threshold) in the first year.

Example Scenario:

- You purchase a qualifying 7,000-lb SUV for $60,000.

- If the Section 179 limit is $1,050,000 (example figure) for the tax year, you could potentially deduct the entire $60,000 in the year you place it in service, assuming over 50% business use.

This immediate write-off can drastically lower your taxable income for that year, allowing you to retain funds or re-invest in your enterprise.

2. Can You Take Section 179 and Bonus Depreciation on Vehicles?

Yes, you can. These two provisions interact, often enabling you to fully deduct the cost of certain qualifying assets in the same year. The typical sequence is:

- Take as much of Section 179 as you desire (up to the maximum limit).

- Apply bonus depreciation (if still available) to any remaining basis.

This strategy is beneficial if you purchase multiple vehicles in a tax year. If you hit the overall Section 179 deduction cap, you may use bonus depreciation to deduct the rest.

3. Luxury Vehicle Caps vs. Heavy Vehicles

Vehicles under 6,000 lbs are frequently referred to as “luxury vehicles” under IRS rules, even if they aren’t particularly opulent or expensive. Such vehicles have more stringent caps on how quickly you can depreciate them. By contrast, heavy vehicles exceeding 6,000 lbs face fewer or no such caps, which is why many entrepreneurs deliberately opt for heavier SUVs, vans, or trucks.

4. SUV Over 6000 Lbs: Benefits and Considerations

A SUV over 6000 lbs can be especially appealing for small businesses due to its versatility and possible tax deductions. However, always consider real-world factors such as fuel efficiency, insurance costs, and maintenance expenses. Just because a vehicle qualifies for an immediate tax deduction doesn’t guarantee it’s the right choice for your business needs.

Steps to Claim Section 179 for Vehicles Over 6,000 lbs

To ensure compliance and optimize your deduction, consider the following step-by-step process:

- Determine Qualifying GVWR

- Look up the manufacturer’s listed Gross Vehicle Weight Rating. Ensure it’s over 6,000 lbs.

- Keep a printed or digital copy of the specification sheet or official documentation as proof.

- Establish Business Use

- Maintain accurate mileage logs showing when and how the vehicle is used for business vs. personal errands.

- You must exceed 50% business use to qualify for Section 179 benefits.

- Separate Personal and Business Expenses

- If you use the vehicle for personal purposes, carefully track those miles.

- Only the percentage of business use is deductible.

- Use expense management or spend management tools to track these expenses effectively.

- Calculate the Deductible Amount

- Determine the portion of the purchase price attributable to business use.

- Deduct up to the applicable Section 179 limit.

- If you still have a remaining basis, consider bonus depreciation.

- File Proper Tax Forms

- Generally, you will use Form 4562 (Depreciation and Amortization) to claim your Section 179 deduction.

- Ensure all relevant sections are accurately completed.

- Retain Documentation

- Keep purchase receipts, financing documents, mileage logs, and other records. Check with a CPA for startups for ways to streamline these systems.

- This helps you if audited or if your business use percentage is ever questioned.

- Monitor Changes in Business Use

- If your vehicle’s business usage drops below 50% in future years, be aware you may need to recapture some of the claimed initial depreciation.

How to Claim Your Deduction

To claim Section 179 benefits on 6000 pound vehicles, fill out the appropriate tax form (Form 4562) and submit it with your annual tax return. Read the instructions thoroughly or partner with a qualified accountant for accurate filings.

If you need more insight, you could visit Section 179 deduction for a step-by-step guide

Key Considerations & Potential Limitations

1. Limitations on High-Cost Vehicles

Although heavy vehicles over 6,000 lbs benefit from fewer “luxury auto” caps, they can still be subject to an overall Section 179 limitation. For example, suppose the IRS sets a maximum Section 179 deduction of $1,160,000 for the year and purchases several heavy vehicles exceeding that total purchase amount. In that case, you cannot exceed the overall Section 179 limit. The remainder might be depreciated using bonus depreciation or the standard Modified Accelerated Cost Recovery System (MACRS) over multiple years.

2. Recapture Rules

Suppose the vehicle’s business usage drops below 50% within the asset’s “recovery period” (often five years for vehicles). In that case, the IRS may require a portion of the initially claimed deduction to be added to your taxable income. This “recapture” helps ensure that Section 179 primarily benefits assets used for genuine business purposes.

3. State Tax Variations

While many states mirror federal depreciation rules, some cap or disallow bonus depreciation, Section 179, or both at certain thresholds. Check whether your state has decoupled from federal Section 179 rules or imposes unique limitations. This can affect your overall strategy.

4. Planning Around the Vehicle Purchase Date

To claim a deduction for a given tax year, your vehicle must be purchased and “placed in service” (i.e., ready and available for business use) before the end of that tax year. If you sign the paperwork on December 28 but don’t pick up the truck until January 2, it may not count for the earlier tax year.

Section 179 Deduction Vehicle List 2024-2025: Updates and Criteria

Every tax year, the rules and dollar limits for Section 179 can change. Make sure you have the Section 179 Deduction Vehicle List 2024-2025 handy to see which vehicles and purchase price caps apply:

- Eligibility Requirements: The vehicle must be new (or new to you), predominantly used for business, and put into service during the tax year.

- Deduction Limits: There are annual caps on how much can be deducted under Section 179. Consult a tax professional or reference the IRS guidelines for exact figures.

- Record-Keeping: Maintain documentation—purchase receipts, proof of GVWR, and mileage logs—to validate your deduction if audited.

List: Section 179 Deduction Vehicles List for 2025 Cars Over 6,000 lbs

Below is a non-exhaustive list of heavier vehicles (based on manufacturer-provided GVWR data) that often meet or exceed the Section 179 vehicle weight threshold of 6,000 lbs. The vehicles listed are grouped by make and model, with approximate GVWR values. Always verify the exact GVWR for the model year you purchase, as these ratings can change.

Note: GVWR (Gross Vehicle Weight Rating) represents the maximum operating weight/mass of a vehicle, including the vehicle’s chassis, body, engine, engine fluids, fuel, accessories, driver, passengers, and cargo, but excluding the weight of any trailers.

| Make & Model Cars Over 6,000 Lbs | Pricing Range Estimate | Approx. GVWR |

|---|---|---|

| Audi Q7 | $60,000 – $75,000 | 6,900 lbs |

| Audi SQ7 | $85,000 – $95,000 | 6,900 lbs |

| Audi Q8 | $70,000 – $85,000 | 6,900 lbs |

| Audi SQ8 | $90,000 – $100,000 | 6,900 lbs |

| BMW X5 xDrive45e | $65,000 – $80,000 | 7,165 lbs |

| BMW X6 M50i | $85,000 – $100,000 | 6,063 lbs |

| BMW X7 xDrive40i | $75,000 – $90,000 | 7,143 lbs |

| BMW X7 M50i | $100,000 – $120,000 | 7,143 lbs |

| BMW X7 M50d | $100,000 – $120,000 | 7,143 lbs |

| Bentley Bentayga | $180,000 – $250,000 | 7,275 lbs |

| Bentley Bentayga Hybrid | $200,000 – $260,000 | 7,165 lbs |

| Bentley Bentayga Speed | $250,000 – $300,000 | 7,275 lbs |

| Bentley Flying Spur | $200,000 – $220,000 | 6,724 lbs |

| Bentley Flying Spur V8 | $210,000 – $230,000 | 6,724 lbs |

| Bentley Flying Spur W12 | $220,000 – $240,000 | 6,724 lbs |

| Bentley Mulsanne | $310,000 – $350,000 | 6,173 lbs |

| Bentley Mulsanne Speed | $335,000 – $370,000 | 6,173 lbs |

| Bentley Mulsanne Extended | $350,000 – $400,000 | 6,617 lbs |

| Buick Enclave Avenir AWD | $55,000 – $60,000 | 6,160 lbs |

| Buick Enclave Avenir FWD | $53,000 – $58,000 | 6,055 lbs |

| Buick Enclave Essence AWD | $50,000 – $55,000 | 6,160 lbs |

| Buick Enclave Essence FWD | $48,000 – $53,000 | 6,055 lbs |

| Cadillac Escalade | $80,000 – $100,000 | 7,100 lbs |

| Cadillac Escalade ESV | $85,000 – $105,000 | 7,300 lbs |

| Cadillac Escalade Platinum | $100,000 – $110,000 | 7,100 lbs |

| Cadillac Escalade ESV Platinum | $105,000 – $115,000 | 7,300 lbs |

| Chevrolet Silverado 1500 | $36,800 – $55,000 | 6,700 – 7,300 lbs |

| Chevrolet Silverado 2500HD | $40,000 – $60,000 | 10,000 lbs |

| Chevrolet Silverado 3500HD | $45,000 – $65,000 | 14,000 lbs |

| Chevrolet Silverado 4500HD | $50,000 – $70,000 | 16,500 lbs |

| Chevrolet Silverado 5500HD | $55,000 – $75,000 | 19,500 lbs |

| Chevrolet Silverado 6500HD | $60,000 – $80,000 | 23,500 lbs |

| Chevrolet Express Cargo Van 2500 | $41,800 – $50,000 | 8,600 lbs |

| Chevrolet Express Cargo Van 3500 | $43,000 – $52,000 | 9,900 lbs |

| Chevrolet Express Passenger Van | $45,000 – $55,000 | 9,600 lbs |

| Chevrolet Suburban | $60,000 – $80,000 | 7,800 lbs |

| Chevrolet Tahoe | $55,000 – $75,000 | 7,400 lbs |

| Chevrolet Traverse | $35,000 – $50,000 | 6,160 lbs |

| Chrysler Pacifica | $44,145 – 55,930 | 6,055 lbs |

| Chrysler Pacifica Hybrid | $52,750 – $61,480 | 6,300 lbs |

| Dodge Durango (SRT, Citadel, R/T, GT, SXT) | $45,000 – $85,000 | 6,500 lbs |

| Ford Expedition | $65,000 – $85,000 | 7,450 lbs |

| Ford Expedition MAX | $70,000 – $90,000 | 7,700 lbs |

| Ford F-150 | $30,000 – $70,000 | 6,100 – 7,850 lbs |

| Ford F-250 Super Duty | $40,000 – $60,000 | 10,000 lbs |

| Ford F-350 Super Duty | $45,000 – $65,000 | 14,000 lbs |

| Ford F-450 Super Duty | $59,995 – $94,035 | 16,500 lbs |

| Ford F-550 Super Duty | $63,220 – $73,610 | 19,500 lbs |

| Ford Transit Cargo Van T-250 HD | $51,885 – $53,000 | 9,070 lbs |

| Ford Transit Cargo Van T-350 HD | $70,395 – $78,095 | 10,360 lbs |

| Ford Transit Passenger Wagon | $56,400 – $65,900 | 10,360 lbs |

| GMC Sierra 1500 | $37,000 – $55,000 | 6,800 – 7,200 lbs |

| GMC Sierra 2500HD | $40,000 – $60,000 | 10,000 lbs |

| GMC Sierra 3500HD | $45,000 – $65,000 | 14,000 lbs |

| GMC Sierra 3500HD Denali | $85,385 – $98,195 | 14,000 lbs |

| GMC Sierra 4500HD | $50,000 – $70,000 | 16,500 lbs |

| GMC Sierra 5500HD | $55,000 – $75,000 | 19,500 lbs |

| GMC Sierra 6500HD | $60,000 – $80,000 | 22,900 lbs |

| GMC Yukon | $60,000 – $80,000 | 7,300 lbs |

| GMC Yukon XL | $65,000 – $85,000 | 7,800 lbs |

| Honda Odyssey | $43,670 – $52,630 | 6,019 lbs |

| Infiniti QX80 | $70,000 – $90,000 | 7,385 lbs |

| Jeep Grand Cherokee (including SRT, L) | $40,000 – $70,000 | 6,500 lbs |

| Jeep Wrangler Unlimited | $36,695 – $51,455 | 6,500 lbs |

| Jeep Gladiator Rubicon | $51,100 – $61,100 | 6,250 lbs |

| Land Rover Defender 110 | $60,800 – $152,000 | 7,165 lbs |

| Land Rover Defender 90 | $56,900 – $109,800 | 7,055 lbs |

| Land Rover Discovery | $60,200 – $79,800 | 7,165 lbs |

| Land Rover Discovery Sport | $48,900 – $53,100 | 6,724 lbs |

| Land Rover Range Rover | $107,900 – $209,000 | 7,165 lbs |

| Land Rover Range Rover Sport | $83,700 – $180,700 | 7,165 lbs |

| Land Rover Range Rover Evoque | $49,900 – $54,900 | 6,724 lbs |

| Land Rover Range Rover Evoque R-Dynamic | $49,900 – $54,900 | 6,724 lbs |

| Lexus LX 600 | $106,850 – $115,850 | 7,230 lbs |

| Lexus LX 700h | $115,350 – $141,350 | 7,452 lbs |

| Lexus GX 550 | $64,250 – $81,750 | 7,165 lbs |

| Lexus TX 350h | $56,490 – $65,760 | 6,010 lbs. |

| Lexus TX 500h | $55,140 – $71,810 | 6,315 lbs |

| Lexus TX 550h+ | $78,560 | 6,540 lbs |

| Lincoln Aviator | $58,495 – $86,995 | 6,001 lbs |

| Lincoln Navigator | $101,990 – $119,490 | 7,200 lbs |

| Mercedes-Benz GLS 580 4MATIC | $109,863 – $148,870 | 6,768 lbs |

| Mercedes-Benz GLS 600 4MATIC | $181,360 – $244,045 | 6,768 lbs |

| Mercedes-Benz G 550 4×4 Squared | $148,250~ | 7,057 lbs |

| Mercedes-Benz AMG G 63 4MATIC SUV | $187,250 to $315,220 | 6,724 lbs |

| Mercedes-Benz Sprinter Cargo Van | $50,830 – $59,980 | 9,050 – 12,125 lbs |

| Nissan Armada 2WD/4WD | $56,520 – $79,990 | 7,300 lbs |

| Nissan Titan 2WD S | $45,000~ | 7,300 lbs |

| Nissan NV 1500 S V6 | $30,000 – $35,000 | 8,550 lbs |

| Nissan NVP 3500 S V6 | $40,000 – $45,000 | 9,100 lbs |

| Porsche Cayenne Turbo Coupe | $161,500 – $203,800 | 6,173 lbs |

| Porsche Cayenne Turbo S E-Hybrid Coupe | $179,455 – $185,465 | 6,173 lbs |

| Porsche Cayenne Turbo S E-Hybrid | $157,000 – $185,465 | 6,173 lbs |

| Porsche Panamera Turbo S E-Hybrid | $228,495 – $248,395 | 6,244 lbs |

| Tesla Model X | $79,990 – $94,990+ | 6,000+ lbs |

| Toyota Tundra 2WD/4WD | $40,090 – $75,365 | 6,800 lbs |

| Toyota 4Runner 2WD/4WD LTD | $55,400 – $57,400 | 6,300 lbs |

| Toyota Land Cruiser | $57,900 – $63,900 | 6,725 – 6,835 lbs |

| Toyota Sequoia | $50,000 – $70,000 | 7,200 lbs |

| Volkswagen Atlas | $38,200 – $53,205 | 6,001 lbs |

| Volvo XC90 | $58,450 – $80,700 | 6,200 lbs |

This table references popular makes and models that may qualify under Section 179 if used primarily for business. Because manufacturer specifications can differ each model year, confirm you have the correct year’s data before purchasing. Always conduct your own research and consult with your small business CPA to ensure eligibility and compliance with tax regulations.

Popular 6000 Pound Vehicles

Common 6000 lb vehicles include many large SUVs, pickup trucks, and cargo vans. Business owners pay special attention to these models because of their favorable tax treatment under Section 179. If you’re searching online, you might come across terms like cars over 6000 lbs, 6000 lb cars, or vehicles over 6000 pounds—all of these refer to the same category of heavy-duty automobiles.

Cars Over 6000 Pounds and Section 179

The IRS allows businesses to claim an accelerated depreciation for cars over 6000 pounds. These are often heavy-duty SUVs, trucks, or vans. When your vehicle meets the 6,000-pound threshold, it typically qualifies for enhanced depreciation benefits compared to lighter vehicles.

Frequently Asked Questions

Can I get a tax write-off for a vehicle over 6,000 lbs?

Answer: You can typically obtain a tax deduction for a qualifying vehicle over 6,000 lbs by leveraging Section 179 deduction for vehicles over 6000 lbs. The key is ensuring that the vehicle is used more than 50% for business, meets the GVWR threshold, and is purchased (not leased) and placed in service during the year you claim the deduction.

What is the difference between Section 179 and vehicle bonus depreciation?

- Section 179: Allows you to expense up to the allowable annual maximum in the year the vehicle is placed in service. It has a strict business-use requirement of over 50%.

- Bonus depreciation: Generally applies after Section 179, allowing you to deduct a significant remaining portion of the purchase price (if any basis remains). Bonus depreciation often does not require the same 50% threshold, but it still requires the asset to be new or “first use” in many cases (though there can be exceptions for used property if certain conditions are met).

Is there a limit on the Section 179 deduction for vehicles over 6,000 lbs?

Answer: Yes. While heavier vehicles can often be fully expensed, you’re still subject to the overall annual Section 179 limit (which changes yearly). If the total cost of all qualifying property, including heavy vehicles, exceeds that limit, you can’t deduct above that amount under Section 179. You may, however, use bonus depreciation to write off additional amounts, subject to the applicable rules.

Does Section 179 apply to used vehicles?

Answer: Often, yes. Does section 179 apply to used vehicles? If the vehicle is new to your business, meets the necessary usage criteria (primarily business use over 50%), and you haven’t previously taken a Section 179 deduction on that asset, it can qualify.

How does Section 179 work for vehicles with personal use?

Answer: You must keep track of business vs. personal miles. If you use a qualifying vehicle 70% for business, you can only expense 70% of its cost under Section 179. Should your company use fall below 50% in subsequent years, you may face recapture of a portion of the deduction.

What if I buy multiple heavy vehicles in the same year?

Answer: You can claim Section 179 for multiple qualifying vehicles in the same year, provided you remain under the total Section 179 expense limit, and each vehicle is used over 50% for business. If your total purchase cost exceeds the maximum Section 179 deduction, bonus depreciation may be employed for the remainder.

Do electric or hybrid heavy vehicles qualify for Section 179?

Answer: It should qualify if the electric or hybrid vehicle is above 6,000 lbs GVWR and meets all other Section 179 requirements. In some cases, you may also be eligible for other green energy credits, though those might interact differently with Section 179 or bonus depreciation. Always consult the latest IRS energy credits guidance when buying an alternative fuel vehicle.

What is the significance of the date I place the vehicle in service?

Answer: To claim the deduction for a specific tax year, the vehicle must be purchased and placed in service (available for regular business use) before the end of that tax year (e.g., December 31 for a calendar-year taxpayer). Merely signing the purchase agreement is not enough if you don’t receive the vehicle and have it available.

Can I claim the Section 179 deduction if I finance my vehicle purchase?

Yes. If you finance the purchase of a qualifying heavy vehicle, you can still claim the Section 179 deduction for the full purchase price (up to applicable limits) in the year the vehicle is placed in service. The fact that you have a loan on the vehicle does not prevent you from taking the Section 179 deduction. You are deducting the cost of the asset, not just the payments made.

What happens if I buy a qualifying vehicle very late in the tax year, like in December? Can I still get the deduction for that year?

Yes, potentially. The key date is not when you purchase the vehicle, but when it is ‘placed in service’ – meaning it’s ready and available for its specific use in your business. If you purchase a vehicle in late December and it is immediately ready and available for business use before December 31st, you can generally claim eligible deductions (like Section 179 and bonus depreciation) for that tax year. Ensure you document the placed-in-service date.

Does Section 179 apply to leased vehicles?

Generally, no, not for the business leasing the vehicle (the lessee). Section 179 is an election to expense the cost of purchased (or financed) property. If you lease a vehicle, your business typically deducts the lease payments as an ordinary business expense over the term of the lease. There are different rules for lessors (the company that owns and leases out the vehicle).

Where exactly do I find my vehicle’s Gross Vehicle Weight Rating (GVWR)

You can usually find the GVWR on a label or sticker located on the inside edge of the driver’s side door (the door jamb). It may also be listed in the vehicle’s owner’s manual or on the vehicle manufacturer’s official website if you search by the vehicle’s specific model or Vehicle Identification Number (VIN).

Can I take Section 179 or bonus depreciation if my business operates at a net loss for the year?

Section 179: No. The Section 179 deduction cannot exceed your business’s net taxable income for the year. It cannot create or increase a net operating loss. However, any unused Section 179 deduction due to this income limitation can generally be carried forward to the next tax year.

Bonus Depreciation: Yes. Bonus depreciation is not limited by your business’s taxable income. You can claim bonus depreciation even if your business has a net operating loss.

What tax year rules apply if I bought a vehicle in 2024 but didn’t place it in service until 2025?

The tax rules, limits, and depreciation rates (including bonus depreciation percentage) that apply are for the year the vehicle is placed in service. So, if it was placed in service in 2025, you would use the 2025 rules (e.g., 40% bonus depreciation for 2025, 2025 Section 179 limits), regardless of when it was purchased in 2024.

Exceptions for Certain Vehicles Under Section 179

Do all vehicles over 6,000 pounds qualify for Section 179 deductions?

No. While many heavy SUVs, trucks, and vans qualify, some vehicles are treated differently under Section 179. Special-use vehicles like ambulances, hearses, and transport vans may have unique tax treatments.

How are ambulances, hearses, and transport vans treated under Section 179?

- Ambulances and hearses are considered specialized business vehicles and typically qualify for full depreciation under Section 179, regardless of GVWR limits.

- Transport vans, such as those used for medical transport or shuttle services, may also be eligible for full deductions but should meet IRS guidelines for business use.

Are there any additional restrictions for these vehicles?

While these vehicles generally qualify for full deductions, the IRS requires that they be used 100% for business purposes to claim the entire Section 179 benefit. Mixed-use vehicles may have deductions reduced accordingly.

Where can I find more information on these exceptions?

Refer to IRS Publication 946 or consult a tax professional to ensure your vehicle qualifies for Section 179 deductions under the latest tax regulations.

Section 179 Recapture Rules for Vehicles

What happens if my business use of the vehicle drops below 50% after taking a Section 179 deduction?

If your vehicle’s business use falls below 50% in a subsequent year, the IRS requires you to recapture (repay) a portion of the deduction previously claimed. You may have to add back some of the deductions as taxable income.

How is the recapture amount calculated?

The IRS will recalculate the depreciation as if you had used regular MACRS depreciation instead of Section 179. The difference between the deduction you initially claimed and what you would have been allowed under MACRS must be added to your taxable income in the year the business use falls below 50%.

What business use percentage is required to keep the entire Section 179 deduction?